Join the Trust It Tuesday Newsletter to get started...

Join the Trust It Tuesday Newsletter to get started...

These emails will help you create your ideal life in the following 8 areas:

These emails will help you create your ideal life in the following 8 areas:

1. Physical2. Financial

3. Relationships

4. Emotional

5. Spiritual

6. Sexual

7. Business/Career

8. Social

1. Physical2. Financial

3. Relationships

4. Emotional

5. Spiritual

6. Sexual

7. Business/Career

8. Social

MEET YOUR CADDIE

Trust It Group Membership

Get Coached. Grow In A Community.

Join the group of soul searching, service-oriented individuals who are changing the world one day at a time.

Every single month you get the chance to receive ongoing mind-blowing insights from Fader. Membership includes direct access to Fader for coaching and support. If you want a low-cost way to receive masterful mentorship, as well as join a community of like-minded people... this is the way.

Click the button below to learn more

What Clients Are Saying

"Fader absolutely amazes me. The energy and confidence he radiates. He is my tuning fork... " - Russ

"My Businesswent from a good company to a great one with Fader"

- Kathy

"I never dreamed the Daddy of the Year course would rock my world like it did." - Paul

Self-Paced Courses

Daddy of the Year Course

Learn How to Get the most Coveted Award on the Planet

People talk about how family is their #1 priority, but they rarely live it. If you want to change this, then join the group. You will be challenged in all the right ways to become the best parent (or grandparent) a kid could ask for.

Click the button below to learn more

Fader's 5 Sequences Course

Discover Your Divine Identity and Create Success In Every Area Of Life

If you feel stuck or want to supercharge your life, this is the course for you. You'll learn how to integrate everything that brings you joy into your life. Discover who you really are (and who you are not) and create a life that is fulfilling and fun.

Click the button below to get instant access to the full 5 Sequence Process

18 Holes of Financial Planning

How to Avoid the Mistakes Most People Make in Their Financial Planning

There are many outdated strategies for managing your money. And if you get caught in one of these "holes" you'll end up losing out big time. This book is here to help you out of the money lies that will keep you stuck.

Click the button below to join the waitlist for when this book comes out:

18 Holes of Mastering Life

1:1 Coaching To Put Your Development Into Hyperdrive

This is Fader's signature 1:1 Coaching Program where he'll walk you through his 18 Holes to Mastering Life. This coaching and program covers every major area of life. Get ready for a total transformation.

Click below to set up a free discovery call to see if this is right for you.

Trust It Trading

Learn How to Trade Stock like a PRO

In 6 weeks learn how to trade stock like a professional. Start earning more money to provide for your family and create a life you love.

Click the button below to learn more

Books

The Billions

Another Perspective on the Plan of Salvation

This book saved my daughter from losing her faith in God and in herself. It's a message about how likely it is that the majority, if not all of our human family, will eventually make it back home to HEAVEN.

Click the button below to get a copy of this life changing book...

Daddy of the Year

The Practice and the Gift of Becoming a Great Dad

Among all the roles you play. The role of DAD is the most important. You win in this area and you win at life. This book will give you the keys and strategies for making that a reality.

Click the button below to get the book!

18 Holes of Financial Planning

How to Avoid the Mistakes Most People Make in Their Financial Planning

There are many outdated strategies for managing your money. And if you get caught in one of these "holes" you'll end up losing out big time. This book is here to help you out of the money lies that will keep you stuck.

Click the button below to get the book!

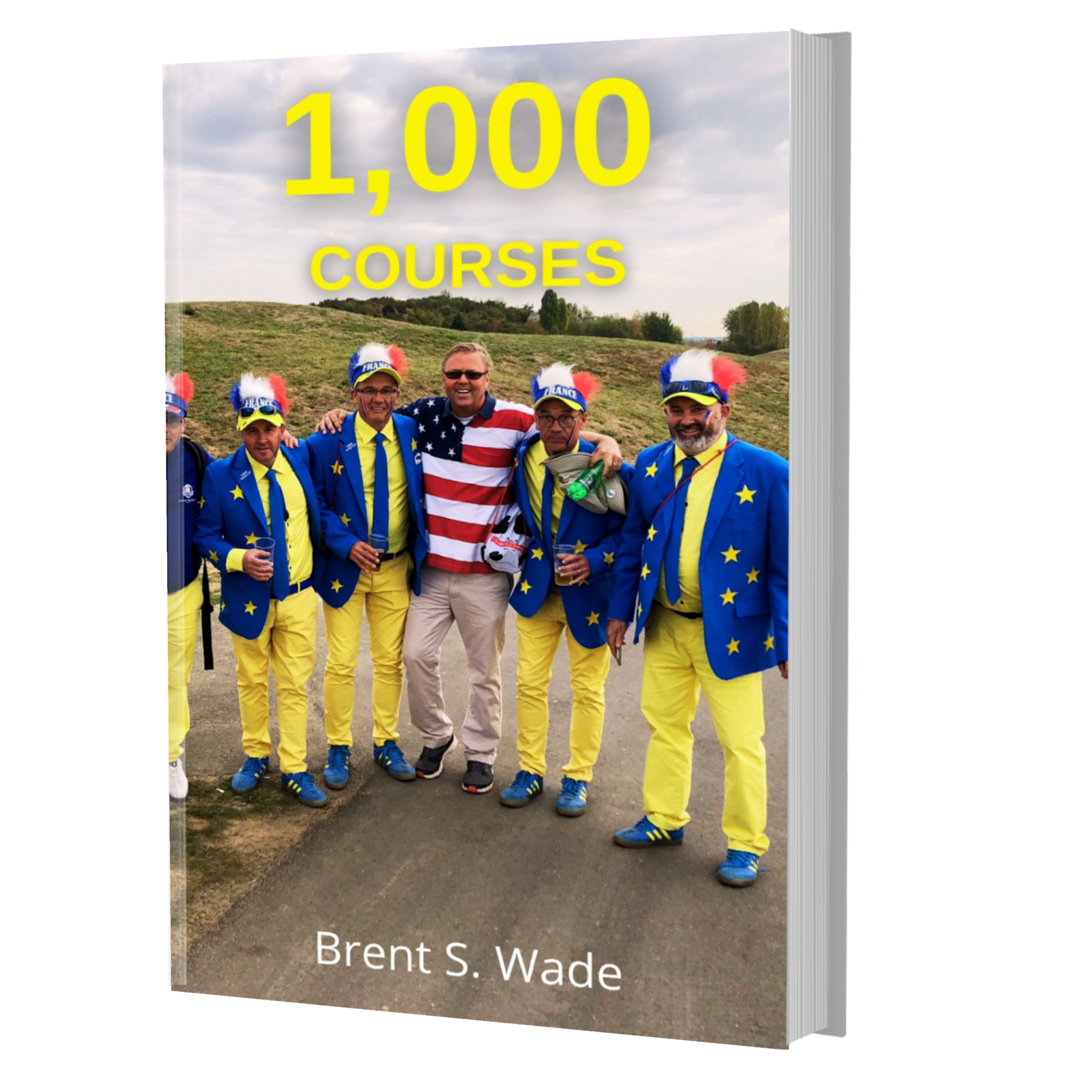

1,000 Courses

What would it be like for you to not only envision a wild and crazy goal, but to actually fulfill it? There are many things we aspire for, but it's rare to find those that have done the impossible. This book will help you unlock your own impossible goal and the strategies to make it happen.

Click the button below to join the waitlist for when this book comes out:

Free Resources

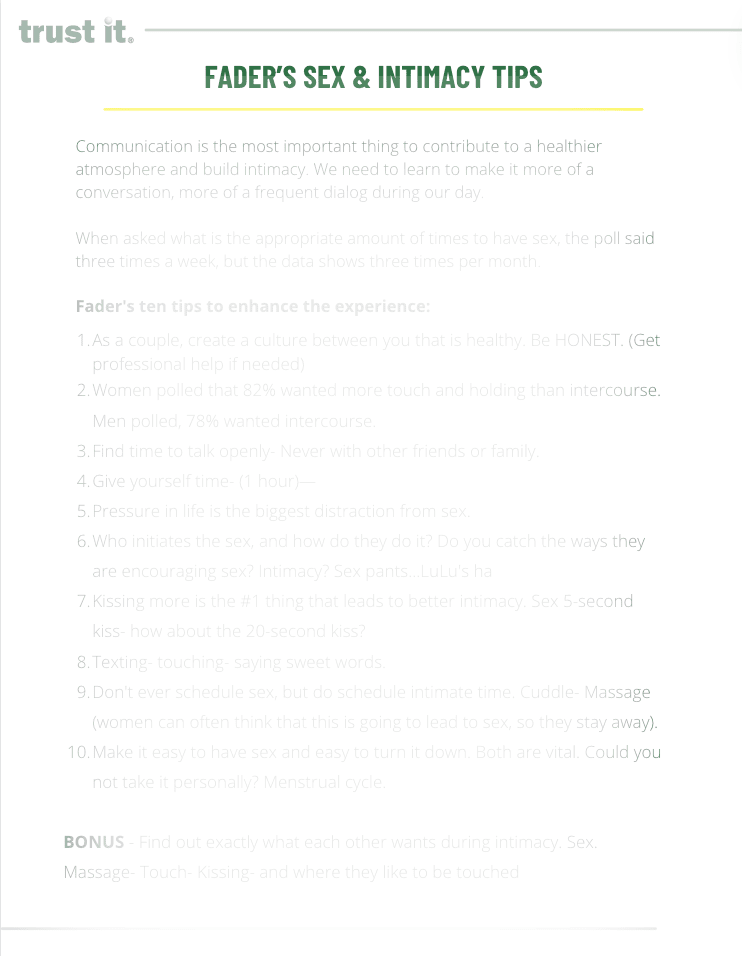

Intimacy can be a tricky thing, but I've distilled the very best insights from years of great intimacy with my wife.

I've put it all together in one sheet you can download by clicking the link below.

Your marriage will thank you...

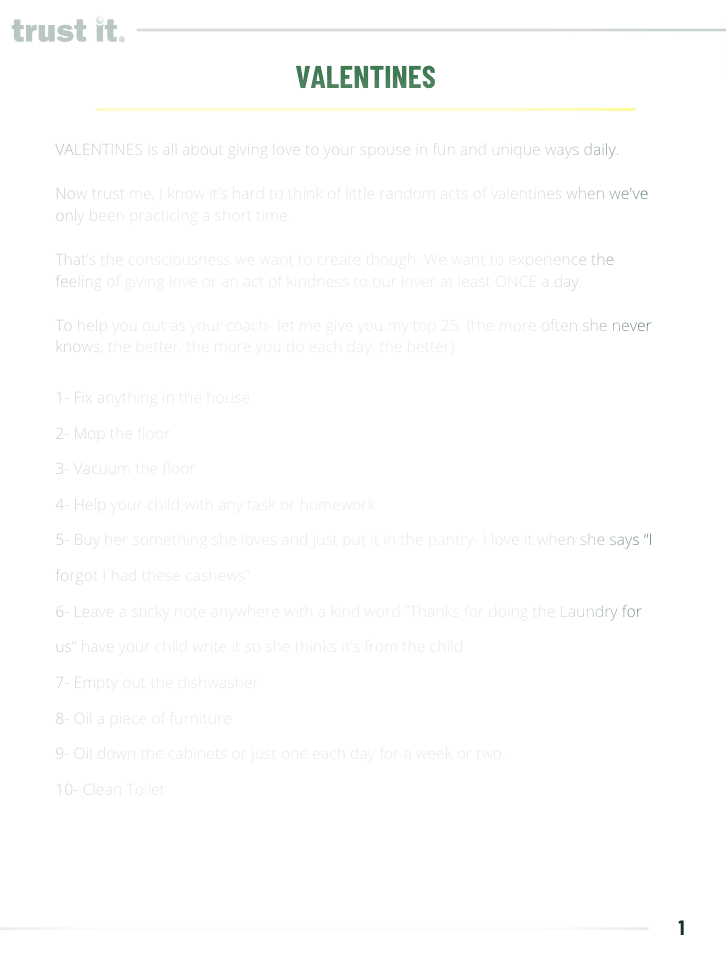

The #1 thing that strengthens my relationship with my spouse is valentines...

This practice isn't what you think, but downloading this one sheet could do more for your relationship than all the books on marriage.

Click below to get the practice...

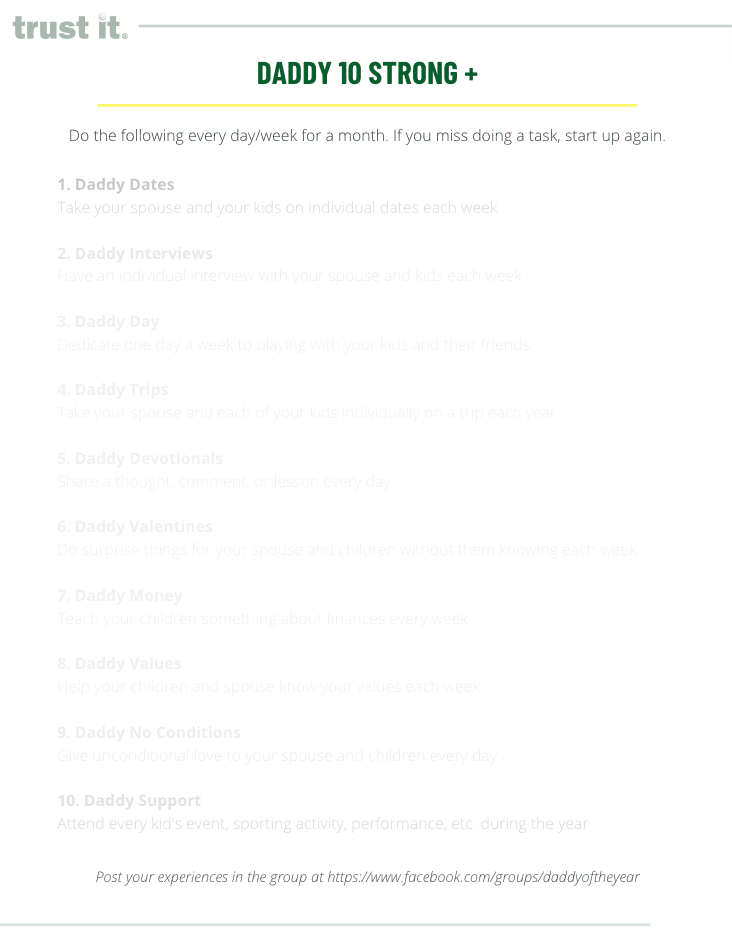

Ever heard of the 75 hard challenge? It's nothing compared to Daddy 10 Strong.

The practices on this sheet will guarantee a great relationship with your kids. The sooner you apply them, the better. It's never too late to be the parent you desire to be.

Download the sheet by clicking the button below.

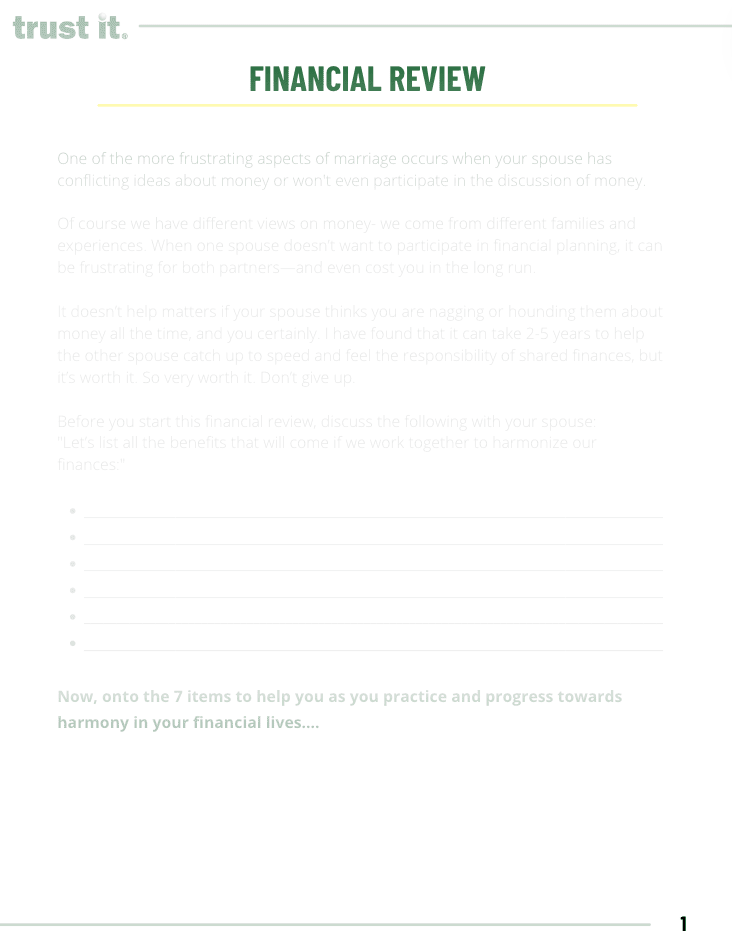

This Financial Review is one of the best tools within my $189 course on Finances.

If you are struggling in this area of your life, download the sheet below to learn the best practices from my 30+ years of financial advising.

Click below to get the practice...

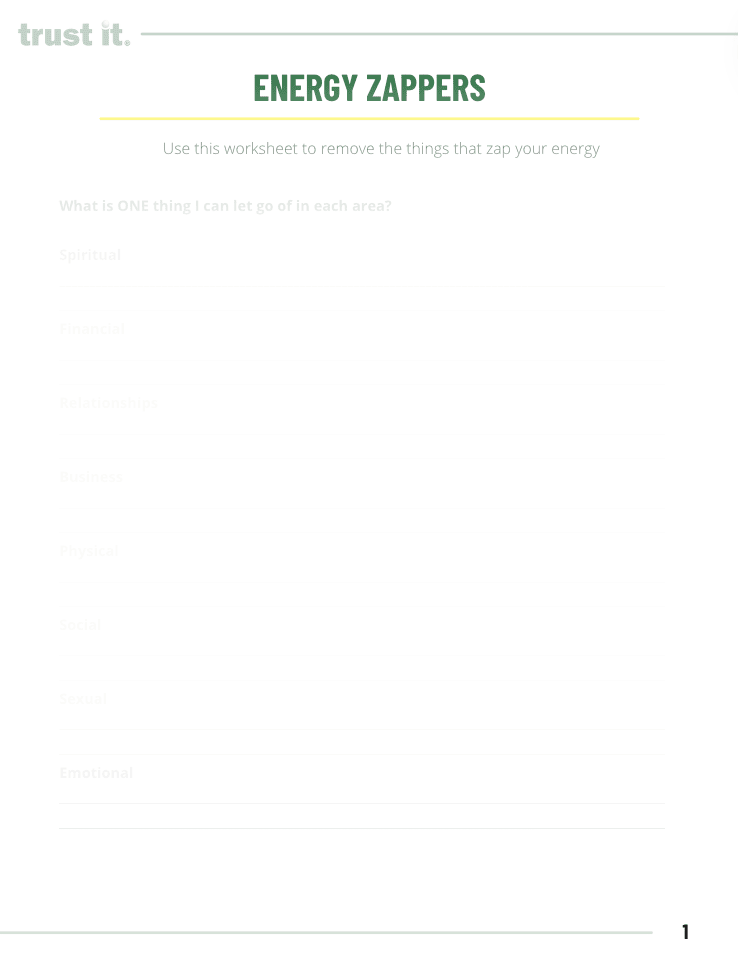

Do you need more energy?

Utilize this worksheet to create more energy in every area of your life.

Download the free sheet by clicking the link below...

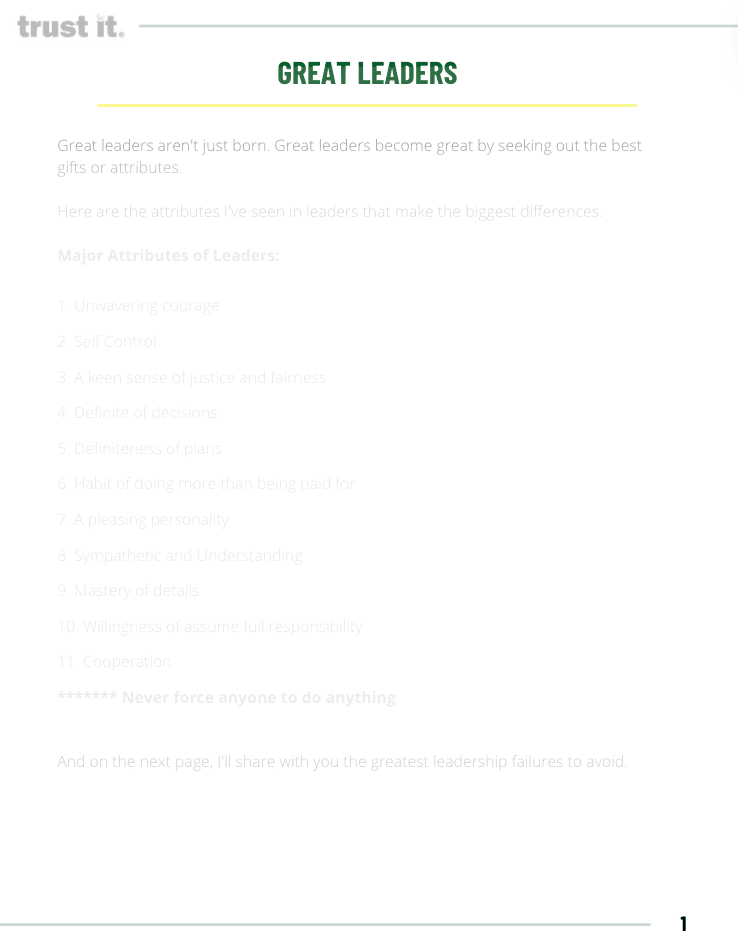

If you want to take your career or business to the next level, then you'll want to download this sheet.

It reveals the best attributes to acquire and the worst failures to avoid as a leader.

Click below to get the sheet...